Safety First: Are Annuities Safe in a Recession? (2026 Guide)

Concerned about market volatility? Learn are annuities safe in a recession, how state guaranty associations protect you, and the best annuity options for 2026.

Financial markets have a way of testing the nerves of the most seasoned investors. As we move through 2026, the primary question for those nearing retirement is simple: are annuities safe in a recession? With memories of past market corrections still fresh and interest rates stabilizing after a volatile period, many Americans are looking for a financial fortress. Annuities, often misunderstood as complex insurance products, are increasingly viewed as a cornerstone for stability. When the economy slows and stock portfolios dip, the contractual guarantees of an annuity can provide a level of security that traditional equity investments simply cannot match.

The Foundations of Annuity Safety

To understand if an annuity is right for your 2026 strategy, you must first understand the layers of protection surrounding these products. Unlike a bank account protected by the FDIC, an annuity is a contract between you and an insurance carrier. This distinction is vital. While there is no federal agency that insures annuities, the insurance industry is structured with multiple tiers of safeguards designed to prevent loss of principal, especially during economic downturns.

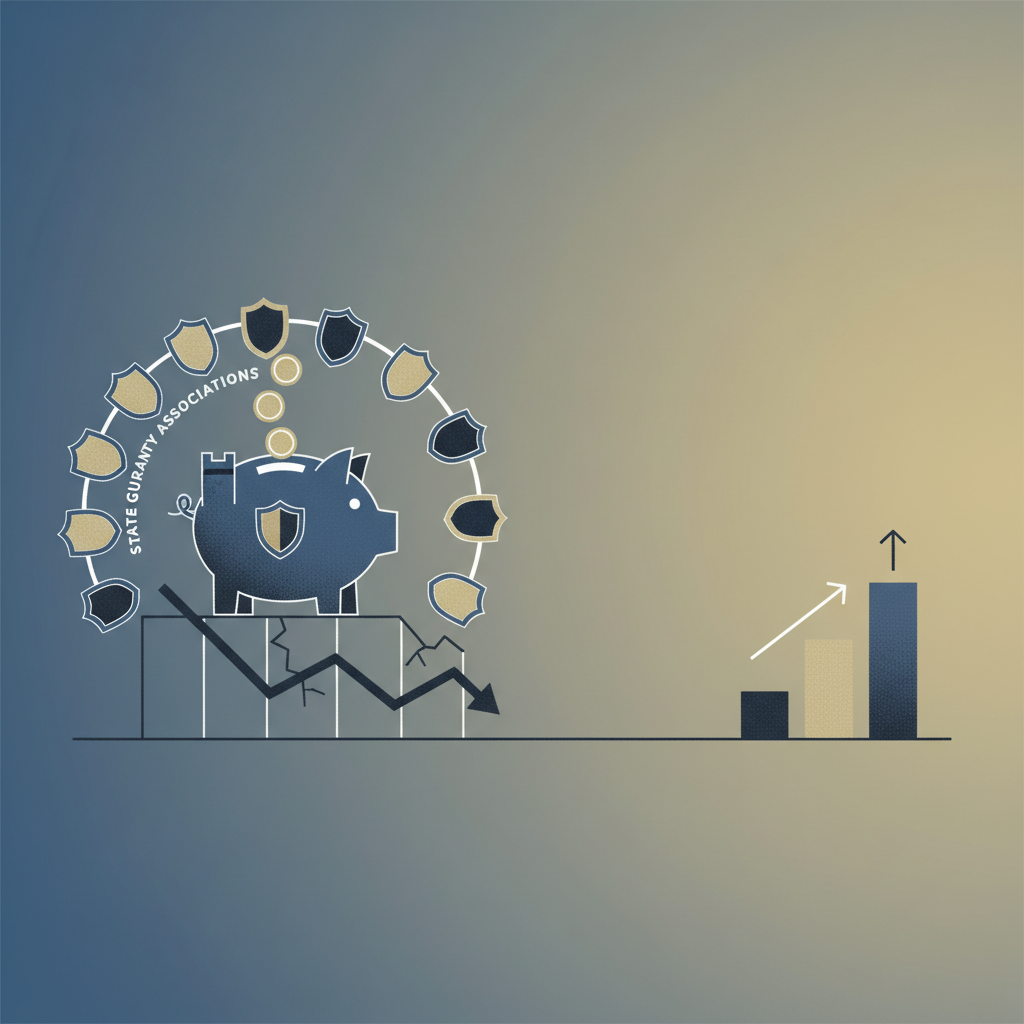

Insurance companies are required by state law to maintain rigorous reserve requirements. According to the National Association of Insurance Commissioners (NAIC), states mandate that insurers hold significant capital in reserve to ensure they can meet every future obligation to policyholders. This regulatory oversight is much stricter than the reserve requirements for many other types of financial institutions. Furthermore, every state maintains a State Guaranty Association. These organizations are funded by insurance companies themselves and step in to pay claims if an individual carrier becomes insolvent. Most states provide coverage between $250,000 and $300,000 for the present value of annuity benefits, according to the National Organization of Life and Health Insurance Guaranty Associations (NOLHIGA).

When asking, "are annuities safe in a recession?" you are really asking two things: Is my money safe if the market crashes? And is my money safe if the insurance company goes bankrupt? The history of the U.S. insurance industry suggests that the answer to both is a resounding yes, provided you select your carrier with care.

Situation: Identifying Your Recession Risk Profile

Before choosing an annuity, you must assess your current financial situation. Most 2026 retirees fall into one of three categories: those who need capital preservation, those who need guaranteed income, and those who want to participate in market growth without the risk of loss.

- The Conservative Saver: This person is likely moving away from riskier assets. They may have already explored high-interest options and are now comparing IRA CD vs Regular CD: Debunking 7 Common Myths in 2026 to see where their tax-advantaged money serves them best. In a recession, their goal is 0% risk of principal loss.

- The Income Seeker: This person needs a monthly check that will not stop, regardless of whether the S&P 500 is up or down. They are often looking for the highest possible payout and might be researching Retirement Planning: How Much Income Will a 500k Annuity Pay in 2026? to calculate their lifestyle budget.

- The Growth Participant: This individual wants some market exposure but needs a floor to prevent losses. They are often weighing the trade-offs between different asset classes, such as Annuity vs Life Insurance Differences: 2026 Retirement Guide, to determine which vehicle offers better long-term protection.

Criteria: How to Evaluate "Safety" in 2026

If you are evaluating annuities as a recession hedge, you should focus on three specific criteria: Credit Ratings, Product Structure, and Liquidity.

#### 1. Credit Ratings (The Insurer’s Health) Safety begins with the carrier. You should only consider companies rated "A-" or better by agencies like A.M. Best or Standard & Poor’s. In a recession, a company with a strong balance sheet is less likely to face liquidity issues. If a company's rating drops during your contract, the state guaranty associations remain your secondary safety net.

#### 2. Product Structure (Protection Against Market volatility) Not all annuities are equally safe in a recession. Fixed annuities and Multi-Year Guaranteed Annuities (MYGAs) are the safest, as they offer a fixed interest rate and a guarantee that your principal will never decrease due to market performance. Fixed Indexed Annuities (FIAs) offer a "floor" (usually 0%), meaning you can never lose money due to market drops, but your gains are capped. Variable annuities are the outlier; because they are tied directly to sub-accounts (similar to mutual funds), you can lose principal in a variable annuity during a recession unless you have purchased an expensive living benefit rider.

#### 3. Liquidity (Access to Cash) Part of safety is having access to your money if an emergency strikes. Most annuities allow for a 10% annual penalty-free withdrawal. However, during a deep recession, you may need more. Understanding the surrender charges—fees for withdrawing more than the allowed amount early—is a critical part of your safety evaluation. If you cannot afford to have your money locked up for 3 to 10 years, an annuity might actually be a risky choice for your personal liquidity.

| Annuity Type | Principal Protection | Income Guarantee | Recession Risk Level |

|---|---|---|---|

| Fixed (MYGA) | 100% Contractual | Guaranteed Rate | Very Low |

| Fixed Indexed | 100% Floor | Participation in Caps | Low |

| Variable | Market Dependent | Rider Required | High |

| Income (SPIA) | Guaranteed Payout | Lifetime Income | Very Low |

| RILA | Partial (Buffer) | Partial Participation | Moderate |

Options: Choosing Your Recession Shield

When we look at the safest annuities for the current economic climate, three specific options stand out for 2026 investors. Each solves a different recession-related fear.

#### The Multi-Year Guaranteed Annuity (MYGA) The MYGA is often called the "insurance version of a CD." It provides a fixed interest rate for a specific term, usually three to ten years. In 2026, MYGA rates have remained competitive with high-yield savings products. According to Bankrate's national survey, yields on fixed-rate products often outperform standard bank instruments during periods of market uncertainty. Because the rate is locked in, a recession actually makes a MYGA more valuable, as it protects your yield while other rates might be falling in response to Fed policy.

#### The Fixed Indexed Annuity (FIA) For those who fear missing out on a market recovery after a recession, the FIA is a popular middle ground. It credits interest based on the performance of a market index, such as the S&P 500. However, the insurer guarantees that the interest credited will never be less than zero. If the market drops 20% in a recession, your account balance stays flat (0%). This makes it a formidable tool for those who want safety but don't want to settle for the lower rates of a traditional fixed annuity.

#### The Single Premium Immediate Annuity (SPIA) If your primary concern is "are annuities safe in a recession" from an income perspective, the SPIA is the gold standard. You trade a lump sum for a guaranteed check for the rest of your life. The insurance company takes on the "longevity risk" and the "market risk." Even if the economy collapses and the insurer’s own investments underperform, they are contractually obligated to pay you. This provides a mental safety net that is hard to quantify during times of financial stress.

Fixed Annuities — Pros & Cons in a Recession

- Principal is contractually protected from all market losses

- Guaranteed interest rates provide predictable growth regardless of economy

- State guaranty associations provide a multi-layered safety net

- High surrender charges limit liquidity during financial emergencies

- Inflation may outpace fixed interest rates over long terms

- Company-specific risk requires vetting of financial strength ratings

Decision: How to Lock in Safety for 2026

Choosing an annuity during a recessionary period requires a shift in mindset from "wealth accumulation" to "wealth preservation." Many investors find that a diversified approach is best. For example, some may choose to ladder their annuities. This involves buying multiple contracts with different maturity dates, similar to how one might research Mastering How to Build a CD Ladder With 50000 in 2026 to ensure regular access to cash and the ability to reinvest at higher rates if they become available.

Another consideration is where the money for the annuity is coming from. If you are moving funds from a volatile brokerage account, make sure you understand the tax implications. It is always wise to consult with a professional who understands the specific 2026 tax codes. Once you have determined that the safety of an annuity outweighs the liquidity of other options, the final step is vetting the insurer. Ensure the carrier's Federal Reserve H.15 data and capital ratios reflect a healthy organization capable of weathering an extended economic storm.

Comparing Annuities to Other "Safe" Assets

In a recession, the competition for your "safe money" usually comes down to annuities vs. CDs vs. Treasury bonds. In 2026, Treasury bonds are often seen as the safest asset because they are backed by the full faith and credit of the U.S. government. However, annuities often provide higher yields than Treasuries because insurance companies invest in a mix of corporate bonds and other private debt that individuals cannot easily access.

Compared to CDs, annuities offer the advantage of tax-deferred growth. While you must pay taxes on CD interest every year, annuity interest is not taxed until you withdraw it. This allows your interest to earn interest, which can be a significant advantage if a recession lasts several years and you want your safe bucket to grow as efficiently as possible.

Understanding the Risks That Still Exist

While we have established that annuities are generally very safe in a recession, they are not "risk-free." No financial product is. The three risks you must still manage are:

- Opportunity Risk: If the market rebounds quickly after a recession and you are locked into a 4% fixed annuity, you might miss out on 20% gains in the stock market. This is why many advisors suggest only putting a portion of your portfolio into an annuity.

- Inflation Risk: If 2026 sees a return to high inflation, a fixed payment may lose purchasing power over time. Some annuities offer inflation protection riders, though these will reduce your initial payout.

- Carrier Risk: While rare, insurance companies can fail. This is why diversifying across two or three different highly-rated carriers is a smart move if you are investing a large sum, such as a million dollars or more.

Final Thoughts for the 2026 Investor

The answer to "are annuities safe in a recession" is a qualified yes. They are safer than stocks, more complex than CDs, and offer unique guarantees that no other asset class can provide. By focusing on fixed products, checking carrier ratings, and understanding the role of state guaranty associations, you can build a retirement plan that stands firm even when the broader economy is on shaky ground. As you move forward, keep your liquidity needs in mind and ensure an annuity is a complement to—not a total replacement for—your liquid savings.

Frequently asked questions

- It is extremely unlikely. State guaranty associations provide a safety net (usually $250k - $300k) and most failing insurers are bought by stronger companies that honor existing contracts.

Related articles

See all →